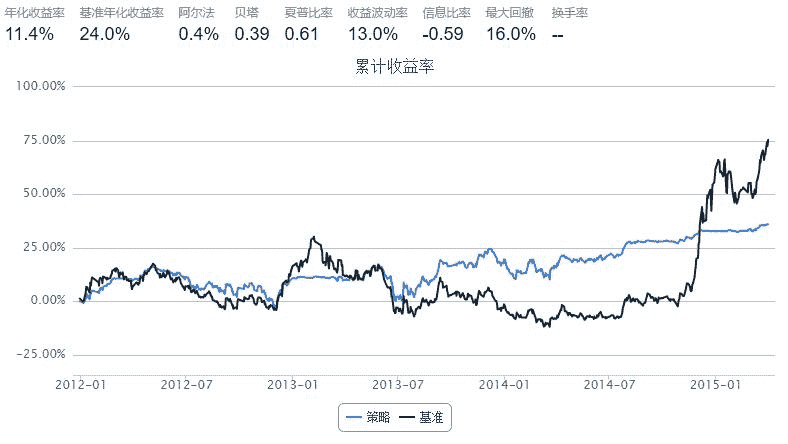

RSI指标策略

来源:https://uqer.io/community/share/549ccfd2f9f06c4bb886323d

策略思路

- 使用talib中的RSI函数计算每只股票过去20天的rsi

- 当rsi低于30是买入,高于70时卖出

- 每只股票仓位最多不超过总资金的10%

import talib as ta

start = '2011-12-01'

end = '2015-04-01'

benchmark = 'SH50'

universe = set_universe('SH50')

capital_base = 5000000

longest_history = 21

def initialize(account):

account.lower_rsi = 30

account.upper_rsi = 70

def handle_data(account):

all_close_prices = account.get_attribute_history('closePrice', longest_history)

rsi, c_price, c_amount = {}, {}, {}

for stock in account.universe:

rsi[stock] = ta.RSI(all_close_prices[stock], longest_history-1)[-1]

c_amount[stock] = account.secpos.get(stock, 0)

for stock in account.universe:

max_amount = int(0.1 * account.referencePortfolioValue / account.referencePrice[stock])

amount = min(int(25000./account.referencePrice[stock]), max_amount - c_amount[stock])

if (rsi[stock] < account.lower_rsi) and (c_amount[stock] < max_amount):

order(stock, amount)

elif (rsi[stock] > account.upper_rsi) and (c_amount[stock] > 0):

order_to(stock, 0)