最经典的Momentum和Contrarian在中国市场的测试

来源:https://uqer.io/community/share/549b5bc8f9f06c4bb8863237

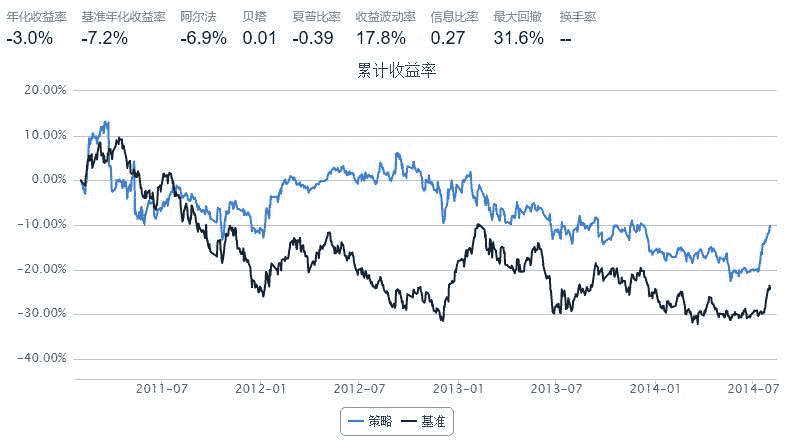

Momentum

策略思路

- Momentum:业绩好的股票会继续保持其上涨的势头,业绩差的股票会保持其下跌的势头

策略实现

- Momentum:每次调仓将股票按照前一段时间的累计收益率排序并分组,买入历史累计收益 最高 的那一组

start = datetime(2011, 1, 1) # 回测起始时间

end = datetime(2014, 8, 1) # 回测结束时间

benchmark = 'HS300' # 使用沪深 300 作为参考标准

universe = set_universe('SH50') # 股票池,上证50

capital_base = 100000 # 起始资金

refresh_rate = 10

window = 20

def initialize(account): # 初始化虚拟账户状态

account.amount = 300

account.universe = universe

add_history('hist', window)

def handle_data(account, data): # 每个交易日的买入卖出指令

momentum = {'symbol':[], 'c_ret':[]}

for stk in account.hist:

if 'closePrice' in account.hist[stk].columns:

momentum['symbol'].append(stk)

momentum['c_ret'].append(account.hist[stk].iloc[window-1,:]['closePrice']/account.hist[stk].iloc[0,:]['closePrice'])

momentum = pd.DataFrame(momentum).sort(columns='c_ret').reset_index()

momentum = momentum[len(momentum)*4/5:len(momentum)]

buylist = momentum['symbol'].tolist()

for stk in account.position.stkpos:

if (stk not in buylist) and (account.position.stkpos[stk]>0):

order_to(stk, 0)

for stk in buylist:

if account.position.stkpos.get(stk, 0)==0:

order_to(stk, account.amount)

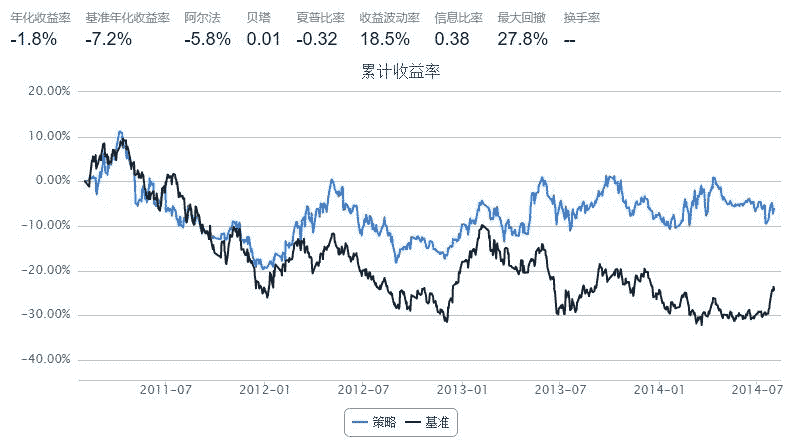

Contrarian

策略思路

- Contrarian:股票在经过一段时间的上涨之后会出现回落,一段时间的下跌之后会出现反弹

策略实现

- Contrarian:每次调仓将股票按照前一段时间的累计收益率排序并分组,买入历史累计收益 最低 的那一组

start = datetime(2011, 1, 1) # 回测起始时间

end = datetime(2014, 8, 1) # 回测结束时间

benchmark = 'HS300' # 使用沪深 300 作为参考标准

universe = set_universe('SH50') # 股票池,上证50

capital_base = 100000 # 起始资金

refresh_rate = 10

window = 20

def initialize(account): # 初始化虚拟账户状态

account.amount = 300

account.universe = universe

add_history('hist', window)

def handle_data(account, data): # 每个交易日的买入卖出指令

contrarian = {'symbol':[], 'c_ret':[]}

for stk in account.hist:

if 'closePrice' in account.hist[stk].columns:

contrarian['symbol'].append(stk)

contrarian['c_ret'].append(account.hist[stk].iloc[window-1,:]['closePrice']/account.hist[stk].iloc[0,:]['closePrice'])

contrarian = pd.DataFrame(contrarian).sort(columns='c_ret').reset_index()

contrarian = contrarian[:len(contrarian)/5]

buylist = contrarian['symbol'].tolist()

for stk in account.position.stkpos:

if (stk not in buylist) and (account.position.stkpos[stk]>0):

order_to(stk, 0)

for stk in buylist:

if account.position.stkpos.get(stk, 0)==0:

order_to(stk, account.amount)