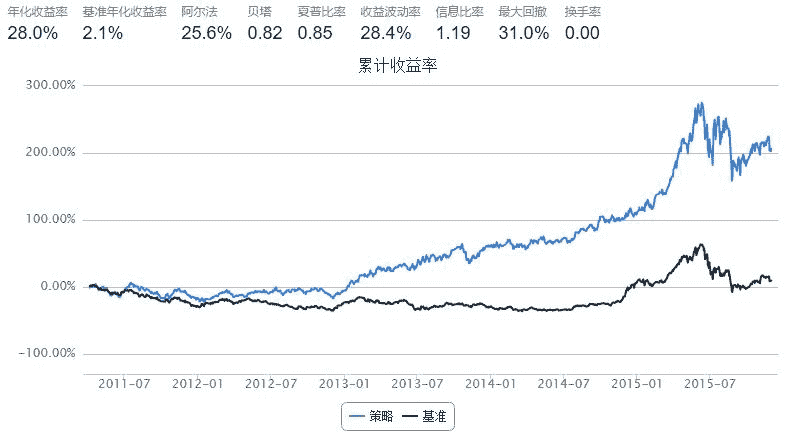

羊驼反转策略

来源:https://uqer.io/community/share/566982a4f9f06c6c8a91b7a2

# 第一步:设置基本参数

start = '2011-04-01' # 回测起始时间

end = '2015-12-01' # 回测结束时间

capital_base = 1000000 # 起始资金

refresh_rate = 10 # 调仓频率

benchmark = 'HS300' # 策略参考标准

freq = 'd' # 策略类型,'d'表示日间策略使用日线回测

# 第二步:选择主题,设置股票池

universe = set_universe('HS300') # 股票池

import numpy as np

import pandas as pd

data=DataAPI.MktStockFactorsOneDayGet(tradeDate='20110331',secID=universe,ticker=u"",field=['secID','REVS10'],pandas="1") #获取start前一日股票池中十日收益

buylist=data.dropna().sort(columns='REVS10',ascending=False).tail(10)['secID'].values.tolist() #将十日收益最差的十只股票组成list

def initialize(account): # 初始化虚拟账户状态

account.stocks_num=10

def handle_data(account): # 每个交易日的买入卖出指令

if account.stocks_num==10: #第一天交易使用buylist

global buylist

account.universe=buylist

hist_prices = account.get_attribute_history('closePrice', 1)

for i in account.universe:

order(i,100000/hist_prices[i][0])

account.stocks_num=1 #之后为非第一天交易策略

sellist=[]

replacelist=[]

sell=DataAPI.MktStockFactorsOneDayGet(tradeDate=account.current_date,secID=account.universe,ticker=u"",field=['secID','REVS10'],pandas="1") #获得十日以来账户中所有股票的收益

sellist.append(sell.min()['secID']) #找出收益最差的股票加入sellist

replace=DataAPI.MktStockFactorsOneDayGet(tradeDate=account.current_date,secID=universe,ticker=u"",field=['secID','REVS10'],pandas="1") #获得股票池中十日以来所有股票的收益

replace=replace.set_index('secID').drop(buylist)

replace=replace.dropna().sort(columns='REVS10',ascending=False).tail(1).reset_index()['secID'].values.tolist() #获得收益最差的股票作为账户中新的代替股票

replacelist.append(replace)

account.universe.remove(sell.min()['secID'])

account.universe=account.universe+replacelist[0]

hist_prices = account.get_attribute_history('closePrice', 1) #获取前一个交易日账户股票价格

for stk in sellist:

order_to(stk,0)

for stk in account.universe:

order(stk,account.cash/10/hist_prices[stk][0])