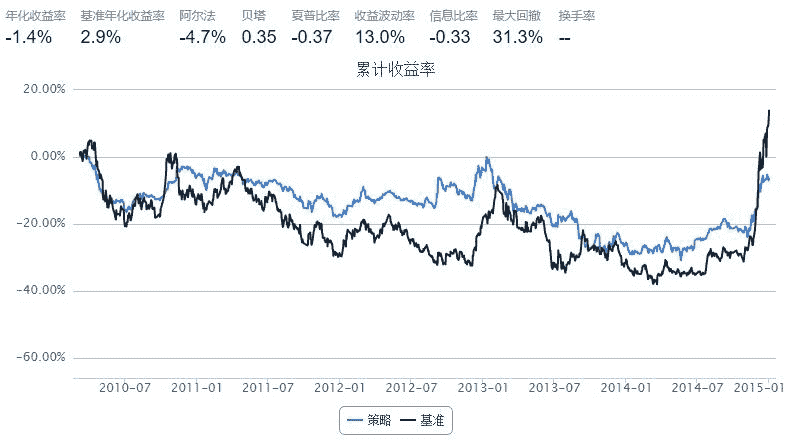

Contrarian strategy

来源:https://uqer.io/community/share/5545ff8df9f06c1c3d68802f

Contrarian strategy similar with Momentum strategy

import pandas as pd

start = '2010-01-01' # 回测起始时间

end = '2015-01-01' # 回测结束时间

benchmark = 'SH50' # 策略参考标准

universe = set_universe('SH50')

capital_base = 100000 # 起始资金

longest_history = 40 # handle_data 函数中可以使用的历史数据最长窗口长度

refresh_rate = 1 # 调仓频率,即每 refresh_rate 个交易日执行一次 handle_data() 函数

def initialize(account): # 初始化虚拟账户状态

pass

def handle_data(account): # 每个交易日的买入卖出指令

returndata = {'symbol':[], 'ret':[]}

history_data = account.get_attribute_history('closePrice',40)

for s in account.universe:

returndata['symbol'].append(s)

returndata['ret'].append(history_data[s][-1] / history_data[s][0])

returndatanew = pd.DataFrame(returndata).sort(columns = 'ret').reset_index()

returndatanew = returndatanew[0:len(returndatanew)/5]

buylist = returndatanew['symbol'].tolist()

for cur in account.valid_secpos:

if cur not in buylist:

order_to(cur,0)

for sym in buylist:

if sym not in account.valid_secpos:

order_to(sym,300)

worse than Momentum strategy